The left needs better tax policy (p.5) - the finale

Deductions... deductions everywhere

In the final part (I, II, III, IV) of this series, let’s talk about tax simplification. The right always talks about tax simplification, but they’re mostly posers. The modern Republican idea of tax simplification is one tax deduction after another. Make car loan interest payments tax deductible, and make tips tax free! This is not a genuine attempt to help lower-income people, nor is it a genuine attempt to make the tax filing process simpler.

Since true tax simplification is up for grabs, the left should bite. Taxes are far too complicated, and there’s a lot of room to simplify. Luckily for the left, this also means the rich will pay far more in taxes.

Tax Expenditures

The easiest path to tax simplification is through greatly reducing ‘tax expenditures.’ Tax expenditures are the list of exclusions, deductions, and credits available to corporations and individuals who file their taxes, and they have a lot of problems.

They complicate our tax-filing process.

They cost the government a lot of money.

They are regressive.

What are tax expenditures?

Let’s start with tax exclusions. A tax exclusion is an amount of income considered ‘pre-tax dollars’ that’s used to determine one’s ‘adjusted gross income’ (AGI). 401(k)s are the best example of this.

Let’s say a person makes $200,000 in a year, but they put $10,000 into their 401(k). They’ll file and pay taxes as if they only made $190,000 (their AGI).

After determining someone’s AGI, they determine their ‘taxable income.’ This is where tax deductions come in. In this case, a ‘deduction’ is a deduction from taxable income.

For example, let’s say our person above, with $190,000 in AGI, paid $20,000 in mortgage interest and property taxes the same year. This person can claim this amount as a tax deduction, reducing their taxable income from $190,000 to $170,000. Even though this person made $200,000, they’re now taxed as if they paid $170,000 because of tax deductions.

You might wonder what makes this different from a tax exclusion. Tax exclusions, barring some exceptions, count before deductions and credits. Meaning, the person who pays tax on $190,000 remains eligible for all deductions and credits after including tax exclusions.

This is important since some tax deductions are only available given a certain amount of adjusted gross income. Lowering one’s adjusted gross income can pull someone into eligibility for other tax deductions.

Finally, after determining someone’s taxable income, they have a tax bill. However, this is a nominal tax bill because they might be eligible for tax credits. A tax credit looks at the tax a person owes and reduces it by the corresponding amount of the credit.

It’s worth noting that tax credits are also ‘refundable’ or ‘non-refundable.’ A person eligible for a refundable tax credit receives the money even if they owe $0 in taxes. Whereas, a non-refundable tax credit can, at most, reduce one’s tax liability to $0.

Let’s use our person above with a taxable income of $170,000. This person owes 20% ($34,000) in taxes, but they qualify for a $4,000, non-refundable, tax credit from energy efficiency improvements they made to their home. The amount they actually pay is now $30,000. After all is said and done, the person above, making $200,000, actually pays $30,000 in taxes, an effective rate of 15%.

In the latest list I could find, there are 170 separate exclusions, deductions, and credits, all of which have their own rules for qualification. Needless to say, this makes the tax filing process much more complicated since individuals might qualify for several different exclusions, deductions, and or credits all at once, and they may or may not qualify for the same things in years ahead. Besides complicating things, let’s move to the other implications of tax expenditures.

The Expense

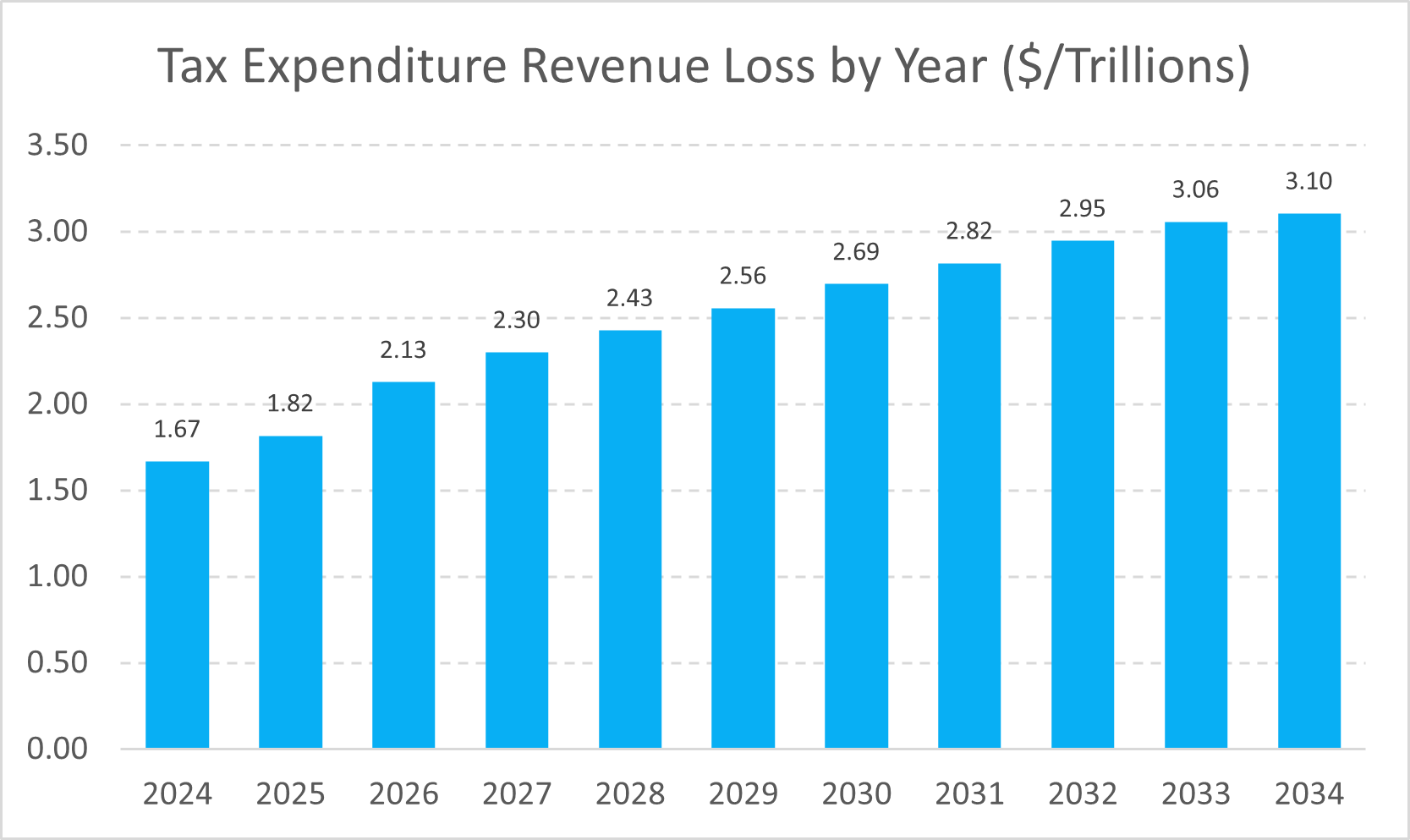

For starters, they cost the government a lot of money.

The government lost $1.67 trillion in revenue in 2024. This is equivalent to over $4,900 for every single American ($1.67t / 340MM).

As a filthy leftist, I’m not intimidated by a program’s high price tag, but tax expenditures are expensive and bad.

Tax Relief for Who?

A big, non-cost, reason tax expenditures are bad is that the rich are disproportionate beneficiaries. Tax expenditures affect income tax liability, and most Americans pay very little, if any, income tax. This is mostly due to the standard deduction, the child tax credit, and the earned income tax credit.

It’s important to understand what the standard deduction is since it explains why a large portion of lower-income Americans don’t benefit from tax deductions (I’ll get to the earned income tax credit later). The standard deduction for individuals in 2024 is $14,600. This deduction is ‘standard’ because it’s effectively the minimum amount a person deducts from their taxable income each year. Every filer qualifies for it, but people have to choose between the standard deduction and claiming the various itemized deductions available.

Therefore, a person choosing an optimal tax planning strategy wouldn’t choose the standard deduction if their itemized deductions are larger than the standard deduction. It’s very rare for a lower-income filer to have itemized deductions greater than the standard deduction, which is why almost all lower-income people choose the standard deduction rather than itemizing.

Even when taking into account tax credits and exclusions, the highest income earners benefit the most. The CBO looked at major tax expenditure buckets in 2019 (more than half of total tax expenditures) and analyzed their distributional consequences.

The top chart looks at the total benefits from major tax expenditures and finds, in aggregate, around 50% of all the benefits go to the top 20% of earners. The big exceptions are the Child Tax Credit, Earned Income Tax Credit, and Premium Tax Credit, which are all means tested.

Tax expenditures are overwhelmingly a giveaway to the highest income earners in society, while also acting as a tax lawyer and tax accountant jobs program. The justification required for the government to create deadweight loss for the benefit of the rich is a high bar, one not met by current tax expenditure policy.

#NotAllTaxExpenditures

But Econoboi, some tax expenditures are morally good! Also, in fact, some tax expenditures incentivize activities that we want people to do!

This is true. We can see some tax expenditures exist likely out of a sense of justice or a goal of pro-social outcomes. For example, in 2024, the U.S. lost about $160 million in revenue from allowing teachers to deduct classroom expenses from their taxes. The same year, the U.S. lost $14 billion by offering a tax credit for those who purchased clean vehicles.

Both goals are sensible. Our education system sometimes forces teachers to pay for supplies for their students out of pocket, and that’s wrong. We also want to incentivize people to purchase clean vehicles because climate change is an escalating disaster we face on a daily basis.

However, the big question for the left is—isn’t there a better way to do these things outside of the annual tax filing system? Teachers shouldn’t have to purchase supplies for their students. The left should advocate for properly supplying public schools instead, and if someone purchases an electric vehicle, send them a check directly. There’s no reason to call it a tax credit and force them to wait for filing season.

The same logic applies to almost every single tax expenditure—they either disproportionately, and unjustifiably, benefit the richest among us, or there’s a better way to provide relief and/or incentivize behavior.

To caveat—every tax code needs some tax expenditures. For instance, in part one of this series, I spoke about the 'expenditure tax,' which makes all investment tax-deductible. This disproportionately benefits the rich, but I pair this expenditure with much higher taxes on the wealthy’s consumption. In contrast, our current tax expenditure system isn’t nearly as thoughtful or distributionally just.

The way forward

Tax expenditures need major change. They are distortionary, inefficient, and disproportionately benefit the wealthy, and they don’t do this on the cheap.

I suggest the following framework as the way forward:

Eliminate most exclusions, deductions, and credits. The only big, notable, exception would be allowing deductions for investments (see part one for a more in-depth explanation of this).

Tax all savings from this and distribute it as a UBI to all adults.

Move this UBI and the child tax credit to the Social Security Administration as a direct, universal benefit.

The Earned Income Tax Credit

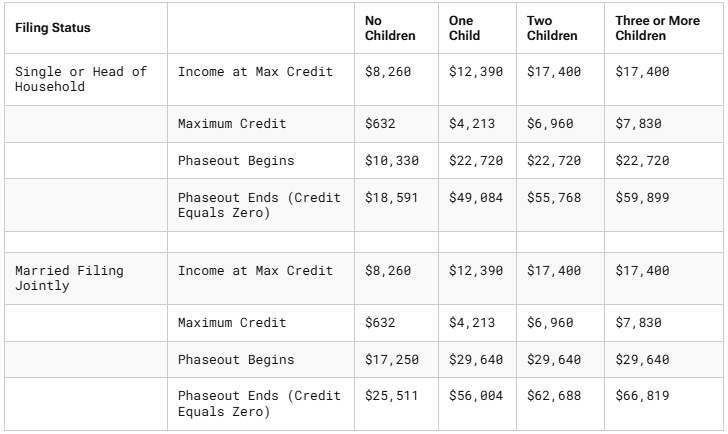

As promised, it helps to explain the earned income tax credit (EITC) in depth. This is something many on the left might be against abolishing because it’s one of the few benefits going towards the lowest income earners. The government accomplishes this by means-testing the EITC. Here is the EITC structure from 2024:

Note three things: (1) the ‘maximum credit’, (2) the effects of having more children, and (3) the lowest earners don’t receive the maximum credit. To visualize the phase-in, see the below chart with 2023 EITC numbers.

Part of the logic of the poorest people not qualifying for the maximum EITC (or any EITC) is to encourage people to move into the labor force. This is cruel in part because it excludes the poorest people from obtaining the credit, and the confusing structure, combined with forcing people to file taxes for the benefit, leads to 20% of people mistakenly failing to claim their benefit.

The lack of universality and the insistence on using the tax code as a means to distribute welfare benefits lead to higher poverty. The EITC’s structure also acts more like a child benefit in the first place, as those without children get almost nothing ($632 in 2024) compared to those with children.

Cash Money

I propose collapsing the EITC and the Child Tax Credit into a single child benefit program administered by the Social Security Administration (SSA).

Matt Bruenig wrote about the advantages of the SSA administering child benefits. In short, the SSA already administers benefits to millions of Americans each month, and the fact that babies receive Social Security cards makes for convenient administration of the new boosted child benefit program.

Using the EITC numbers above, we can calculate the benefits given on a per-child basis in 2024.

Since the EITC exists mostly as a benefit for children, and the child tax credit already exists, we can add these benefits together. The boosted child tax credit for children under 6 years old was $3,600 in 2021. If we adjust that for inflation, the 2024 boosted tax credit would be around $4,000 per child per year.

I would argue it doesn’t make much sense to reduce the amount of the tax credit for each subsequent child since it complicates administration and reduces the anti-poverty effects of the program, so let’s take the maximum monthly child allowance under 2024’s EITC ($351) and add $4,000 annually ($333.33/month).

This comes to just under $700/month per child. This $700/month equals $8,400 per year per child, which is generous, significantly reduces poverty, reduces administrative costs to near zero, and ensures every child receives their benefits independent of their parents’ income or ability to navigate the tax code.

And the childless?

This brings me to people with no kids. The EITC punishes the childless to a radical degree. Under the current EITC, the equivalent per month benefit of someone qualifying for the maximum credit is less than $53/month. Again, this assumes the person makes a high enough income (but not too high) and properly files their taxes.

Investment deductions under the expenditure tax would remain, but there are hundreds of billions of dollars of other deductions that, if eliminated, could form a base for a universal basic income. By removing a lot of the expenditures (subsidies) related to health insurance, local taxes, and capital gains income, we could raise ~$650 billion extra. On a per adult per month basis, this comes to over $200/month ($650 billion / 268.5 million adults).

This $200 is more than the current childless EITC, goes to every adult regardless of income, and, since this is also administered through the SSA, we don’t have to worry about people failing to properly claim the benefit. Every adult citizen with a Social Security number gets the benefit.

Lastly, the new universal basic income and child tax benefit would be part of a person’s taxable income. This might sound odd to tax state benefits, but it’s an effective way to means-test programs under a singular means-testing institution: the IRS. A lot of people want to means-test programs on the front end because we don’t want the rich getting benefits, but that makes the administration of benefits complicated relative to a unified tax code that taxes the rich on the back end.

Say, for example, under a progressive income tax, a single mom with one child receives $8,400 in child benefit, $2,400 in UBI, and she earns a labor income of $30,000. In effect, she pays taxes as if she made $40,800. Let’s say her effective tax rate after the standard deduction is 9%. She pays about $3,600 in taxes but receives $10,800 in benefits. Desegregating this, she effectively pays 9% of her benefits in taxes to the state while receiving a large net-benefit.

Assume the same benefits to a couple making $250,000 in labor income with a single child. They also receive the UBI and child benefit, but their income bracket after the standard deduction has them paying an 18% effective tax rate. They receive the same per-person benefits ($8,400 + $2,400 + $2,400), but they pay over $47,000 in taxes ($250k + 13.2k * 18%). This basic example illustrates why universal benefits with progressive taxation make sense. It’s administratively efficient and ensures a progressive distribution of both income and benefits.

Tax Expenditures

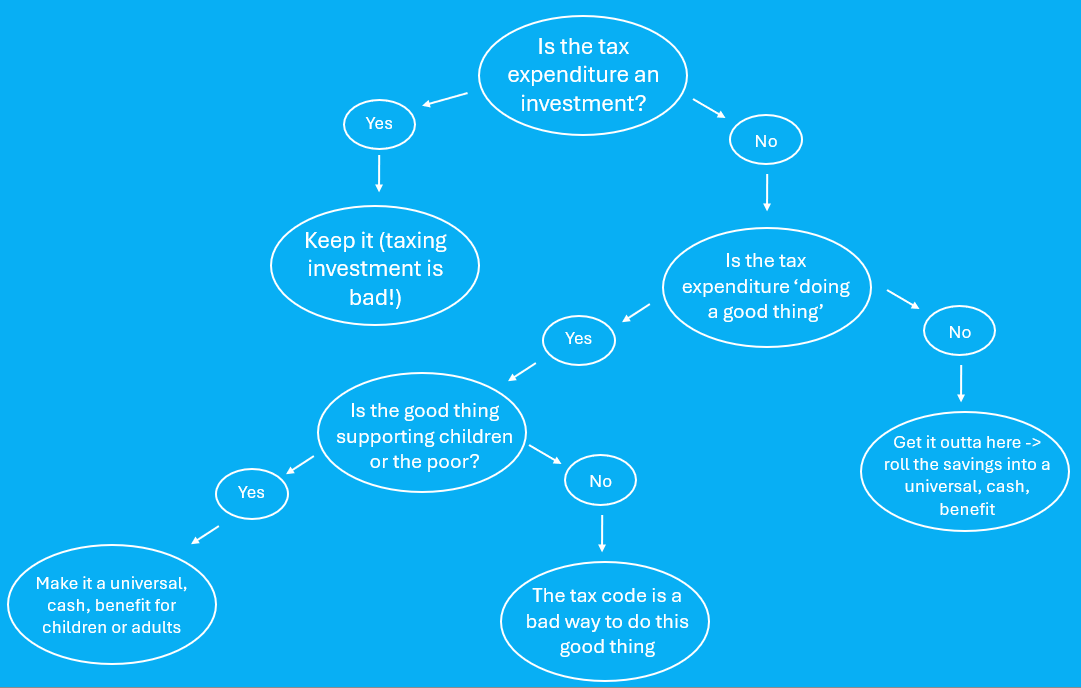

Tax expenditures represent a gigantic bucket of money that the federal government improperly allocates each year. To provide a simple logic chain, I created the following thought tree:

This is a good summary of this article and the general way we on the left should think about tax simplification. There are better ways than the tax code to both do well by vulnerable populations and to incentivize pro-social outcomes. It’s still important to refrain from taxing investment, but progressive rate structures are effective at clawing back money that the wealthy would rather consume on yachts.

For too long, the right has monopolized tax simplification. Ironically, true tax simplification would be a highly progressive distributive policy, and the left should jump at the opportunity.

Series Closing Thoughts

I don’t imagine this will be my last post on tax policy, but I think this is a good point to end on. The five parts in this series serve as a blueprint to raise well-north of 90% of all the revenue society needs to fund the types of expansive institutions, services, and welfare programs the typical leftist wants.

The changes I’ve described in this series accomplish this by making the tax code significantly more economically efficient, more progressive, and simpler. Leftists get a bad rep for being bad on tax policies, and this doesn’t have to be the case. The best taxes available to policy makers are compatible, and directly support, a left-wing disposition.

I hope leftists in the future can adopt the rhetoric and policies of this series, capturing this part of economic discourse for its own means. A world with a tax policy as described in this series is both more egalitarian and abundant, two goals any good leftist should take seriously.

This was a wonderful series. I’ve been a bit despondent about the sometimes lack of genuine policy rigor in some leftist spaces, so it’s awesome to see someone do the hard work. I’m not a leftist my self, but reading the series, the tax changes seem to not only make sense, but we be significantly better and less distortionary than the one we have now. Of course, LVT is everyone’s darling, but the corporation section was a revelation. Thanks!

PS, you might hate this, but Ylesisas wrote a little about taxes, and his broad outline looked a lot like yours: VAT, LVT, removing most tax deductions. Good policy is good policy!

I really liked this series, i was just curious if this has an answer for buy, borrow, die? I suspect the expenditure tax would still be weak against people borrowing against their untaxable wealth. since investments are not taxed.