The left needs better tax policy (p.4)

...and it needs to be popular

Following from part three, the left has a popularity problem, but not with its programs. Most left economic programs are popular. I know there’s some fuzziness with these numbers. Of course the phrasing of questions matters, but that’s another way of saying framing and messaging matters. Most people, in my experience, are not intuitively against things like expanding welfare spending and public services.

These programs are stable or increasing over time in many countries, despite their tax burdens. This doesn’t mean these countries don’t sometimes cut programs, design programs poorly, or fail to offer enough services, but it does mean a message exists that people will buy over a long period of time, even if these programs cost a lot of money.

So, why do I say the left has a popularity problem? It’s because of the cost part. People are very skeptical when a candidate talks about raising taxes or when a government enacts a new tax. The previous three entries (1, 2, 3) of this series are examples of highly optimal taxes, and those taxes could raise enough revenue to fund a radical expansion of social services, but for one reason or another, it may be difficult to get either governments to implement them or politicians to campaign for them.

The left might get hung up on the expenditure tax’s investment deductions. The right might hate to see a 51% top-rate on consumption. The DBCFT is unintuitive and the tariff component is so controversial, even Republicans dropped it in 2017. The land value tax is amazing, and everyone agrees, yet it’s not implemented to its full extent anywhere on the planet because it’s hard to sell to everyday people and politicians.

With this entry, I wanted to point out a couple taxes that aren’t necessarily optimal in their structure, but they have some redeeming qualities. Most notably, these taxes are lower salience and might not stir up the same magnitude of controversy as wonky, optimal, taxes. Consider these taxes strategic options for the left.

Employer-side payroll tax

Let’s start with the employer-side payroll tax. This is a tax employers pay on wages paid to employees. For example, if the employer contribution is 5%, and a worker makes $100,000, the employer pays $5,000 in taxes to the government.

The employer-side payroll tax has some advantages:

It raises a lot of money.

People don’t see the tax, so they don’t mind it as much.

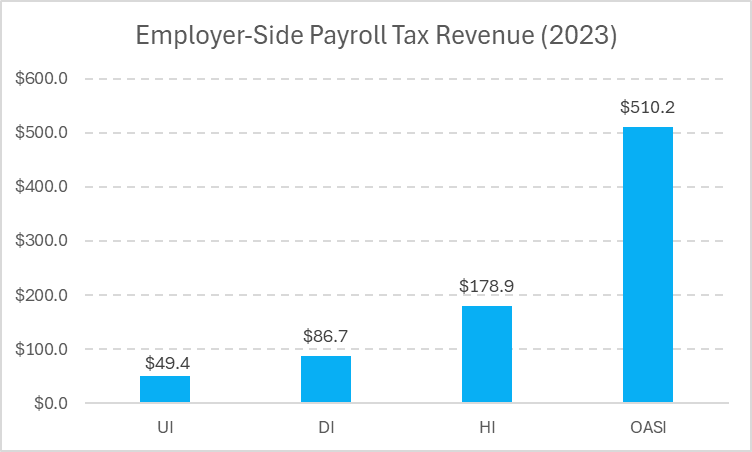

As of 2023, the United States had several employer-side payroll taxes.

Adding the ‘employer rates’ together, we end up with a total employer-side payroll tax of 8.25%. This is a little complicated because of the chart’s note about the boosted 0.9% Medicare tax on high-income individuals and the fact that unemployment insurance contributions change depending on state policy and a company’s employment practices.

Nonetheless, we can look at the aggregate money raised from these taxes, divide OASI, DI, and HI revenue in half (to capture the employer’s share), and add these with the total unemployment insurance revenue to get the total amount the U.S. raises from the employer-side payroll tax.

This is $825 billion dollars going to vulnerable groups of people—the elderly, the disabled, and the unemployed.

This tax raises a lot of money, but it also has a big advantage—employees don’t see any difference in their take-home pay. Sure, we can design a tax code that raises enough money to pay for what we’d like, but the large cost of these programs gives many people pause.

Since corporations mechanically pay the employer-side payroll tax, the left accomplishes two goals at once—we can fund our social programs and make corporations pay for it! This is a sound bite politicians can rely on, and workers won’t mind this as much relative to radical, noticeable, changes in income or sales taxes. Some countries up their employer payroll tax to as high as 26.6%.

Lastly, let’s talk about some important caveats. What some policy wonks will point out is that this tax is actually paid mostly or entirely by labor. Companies accomplish this by, in the long-run, lowering employees’ wages, benefits, and employment opportunities.

In 2007, Sweden had an employer-side payroll tax of over 31%. In order to boost wages and employment for young Swedes, the government cut this rate in half to 15.5% for workers 26 years old or younger. This provided a ripe experimental environment for economists to isolate changes in employer payroll taxes and observe the effects.

The results of the policy were that wages and employment rose.

This chart shows businesses with a high and medium share of young workers. Average wages for both rose overtime, but wages for businesses with a higher share of young workers rose faster, though this was marginal.

This chart shows the employment rate of young people in Sweden by age. The lines are the age cohorts bundled by years. The green and black lines, the years where young people benefited from this policy, show the tax cut reduced youth unemployment by a couple of percentage points.

All this said, even employer payroll taxes double the U.S.’s appear to have marginal effects on wages and employment, but those effects are real, and the design of social programs should compensate for this. For example, most Americans get health insurance from an employer. This costs employers ~$7,500 and ~$19,000 (p.86) per employee for single and family coverage, on average, respectively.

This creates significant friction in the labor market, higher unemployment, deadweight loss, and lower worker wages, similar to an employer-side payroll tax. The only difference is we lose out on the efficiencies of both universal coverage and frictionless labor movement from people no longer needing insurance through an employer.

America also spends over $300 billion on health-related tax subsidies each year. These things combined mean a transition to a universal public-insurance system not tied to employers and paid for with an employer-side payroll tax, would likely save the economy money, administrative inefficiency, and result in pro-employment outcomes.

At the very least, the argument, by framing the inefficiencies of the current system, is very reasonable, even if, all else equal, an employer-side payroll tax is not as perfect as an expenditure tax, DBCFT, or land value tax.

Value-Added Tax (VAT)

Another tax that could survive political scrutiny, if enacted properly, is the value-added tax. The value-added tax is a consumption tax on the ‘value add’ of each step in a production process.

For example, let’s say the VAT rate is 20%, and a refinery purchases $10 worth of gold ore to process for gold bars. They pay $10 for the ore and $2 in VAT ($12 total). Then the refinery sells refined gold bars to a retail outlet for $20. The retail outlet pays $20 for the gold bars and $4 in VAT ($24 total). Finally, the retail customer buys the gold bar for $40 and pays $8 in VAT ($48 total).

Every supplier in the process collects the taxes owed to the government and receives a tax credit for any VAT they paid. This is why it’s a ‘value-added’ tax. Taxes are only paid on the ‘value-added’ of each stage in the production process. The end-consumer doesn’t get a tax credit for VAT paid, meaning the VAT ends up hitting the final consumption base.

Assuming retail customers end up paying the VAT on their purchases, why do I say a VAT could survive political scrutiny? People hate sales taxes after all! Well, many countries require prices to include the VAT. Instead of a bundle of bananas showing $2, and then customers paying $2 + 20% at the register, the price says $2.40, and the customer pays $2.40 at the register.

This is useful for many who strictly budget since they can sum their purchases without needing an in-depth knowledge of retail tax rates and their various exceptions. This is also useful because it lowers the salience of the tax. People, psychologically, do not like seeing taxes paid, but they often appreciate the services they pay for.

The overwhelming majority (175) of countries have a VAT, some charging north of 25%. The CBO estimated a broad base 5% VAT rate in the U.S. would raise $230 billion in 2026. Assuming the U.S. also passed a law requiring retail outlets to include the VAT in prices, policy makers could dedicate this revenue to a specific purpose (like healthcare or retirement services) and raise the rate overtime as costs increase or policy makers transition a program’s funding from one tax to another.

Closing Thoughts

Some will say attempts to lower the salience of taxation is an attempt to mislead, but I disagree. People not liking to see taxes they pay doesn’t mean they don’t like the programs the taxes fund, and it doesn’t mean people pay taxes absent a democratic process and transparent administration. So long as governments engage in democratic and transparent processes to enact new taxes, I don’t see any problem with attempts to lower the salience of taxation. The taxes I mentioned are not all the lower salience taxes available, but they’re two big examples.

These taxes are also, by no means, perfect. The employer-side payroll tax has its problems, but, if given the choice between having no universal healthcare and no employer-side payroll tax or having universal healthcare and an employer-side payroll tax, on balance, the left should prefer the latter.

In general, the messaging of taxation in political campaigns is challenging for members of the left, and perhaps low-salience taxes like this are easier to include in a political platform. Either that, or the left can enact their social programs while in office and hope not to pay a political price for the combination of taxes and spending they enact. After all, it seems with social programs, though they’re paid for with taxes, they’re often popular once people start seeing the benefits of these programs.

Finally, the taxes I proposed in the first three parts are not politically dead in the water. There is a compelling political message with each of these taxes that could be successful if politicians had the courage to act. The entries in this list are just a couple examples of taxes that are fine taxes in and of themselves with robust histories of enactment across countries and time. Maybe the U.S. could follow-suit and enact or expand these taxes at home, with the right set of policy goals in mind.